Chap 9.

상관분석과 회귀분석

9.2 Correlation

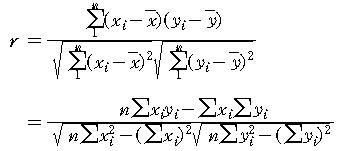

- Def. The sample correlation coefficient for the n pairs

(x_1, y_1), ..., (x_n, y_n) is

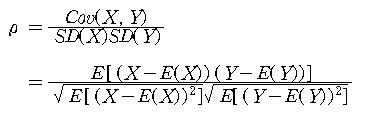

- The population correlation coefficient \rho is a parameter

or population characteristic, so we can use the sample correlation

coefficient to make various inferences about \rho, In particular, r is

a point estimate for \rho, and the corresponding estimator is

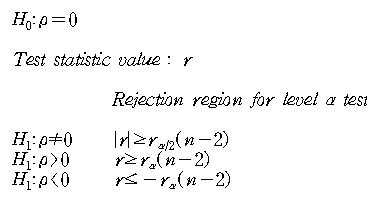

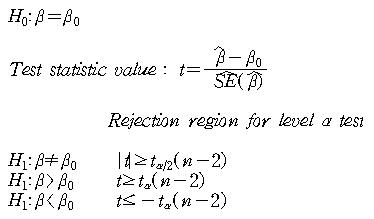

- Procedure for Testing H_0 : \rhp=0

9.3 Simple Linear Regression Analysis

- There exist parameters \alpha, \beta, and \sigma^2 such that for any

fixed value of the independent variable x, the dependent variable is related

to x through the model equation

The quality \epsilon in the model equation is a random variable, assumed to be

normally distributed with E(\epsilon)=0 and V(\epsilon)=\sigma^2.

- More generally the variable whose value is fixed by the experimeter will

be denoted by x and will be called the independent variable.

- For fixed x the second variable will be random; we denote this random

variable and its observed value by Y and y, respectively, and refer to it as

the dependent variable.

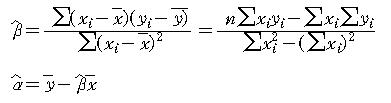

- The least squares estimates of the coefficients \alpha and \beta

of the regression line are

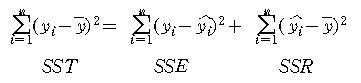

- The ith predicted value, denoted by \hat y_i, is \hat y_i = \hat \alpha + \hat \beta x_i(i=1,...,n), and the ith residual is y_i - \hat y_i.

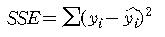

- The error sum of squares, denoted by SSE,

and the estimate of \sigma^2 is

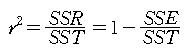

- The coefficient of determination denoted by \rho^2, is given by

- The total sum of squares

- coefficient of determination (

회귀직선의 기여율)

9.4 Inferences about the Simple Linear Regression

- \beta : population regression coefficient (

모회귀계수)

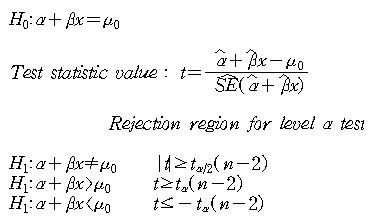

평균반응 \alpha+\beta x

에 관한 추론

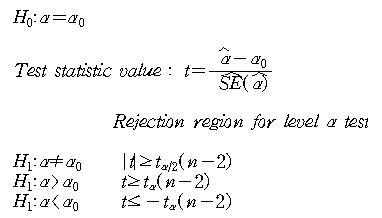

절편 \alpha에 관한 추론

9.5 Analysis of residuals

- 표준화된 잔차인 \hat e_i,s = (y_i - \hat y_i) / \hat sigma들이 마치 표준정규분포

에서의 n개의 서로 독립인 관측값과 유사하게 나타나는가를 검토한다.

Email: lbg@kowon.dongseo.a

c.kr

|