Chap 7.

ĂßÁ¤(Estimation)

7.1~3 Some General Concepts of Point Estimation

- Def. A statistc is any function of the random variables constituting one or more samples, provided that the function does not depend on any unknown parameter values

- Def. A point estimate of a parameter \theta is a single number that can be regared as the most plausible value of \theta

- Def. A point estimator \hat \theta is said to be an unbiased estimator of \theta if E(\hat \theta)=\theta for every possible value of \theta

- Prop. X~Bin(n,p), the sample proportion \hat p=X/n is an unbiased estimator of p.

- Prop. Let X_1,X_2, ..., X_n be a random sample from a distribution with mean \mu, then \bar X is an unbiased estimator of \mu. If in addition the distribution is continuous and symmetric, then \tilde X and any trimmed mean are also unbiased estimator of \mu.

- Prop. Let X_1,X_2, ..., X_n be a random sample from a distribution with mean \mu and variance \sigma^2 . Then the estimator \hat \sigma^2=S^2=\sum_{i=0}^{i=n}(X_i-\bar X)^2/(n-1) is an unbiased estimator of \sigma^2.

- Def. Among all estimators of \theta that are unbiased, choose the one that has minimum variance. The resulting \hat \theta is called the unbiased minimum variance estimator(UMVE) of \theta.

- Def. The standard error of an estimator \theta is its standard deviation sqrt(V(\hat \theta)).

7.4 Interval Estimation Based on a Single Sample

7.4.0 Basic Properties of Confidence Intervals

- Def. A 100(1-alpha)% confidence interval for mean \mu of a normal population when the value of \theta is known is given by

7.4.1 Large-Sample Confidence Intervals for a Popoulation Mean

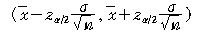

- Prop. If n is sufficiently large, Z=(\bar X - \mu)/(S/sqrt(n)) has approximately a standard normal distribution. This implies that

is a large-sample confidence interval for \mu with confidence level approximately 100(1-\alpha)%. is a large-sample confidence interval for \mu with confidence level approximately 100(1-\alpha)%.

7.4.2 A confidence Interval for the Mean of a Normal Population

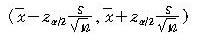

- Assumption. The population of interest is normal, so that X_1, X_2, ... ,X_n constitutes a random sample from a normal distribution with both \mu and \sigma unknown.

- Thm. the random variable T=(\bar X - \mu)/(S/sqrt(n)) has a probability distribution called a t distribution with n-1 degree of freedom.

- Not. Let t_\alpha(n) = the number on the measurement axis for which the area under the t curve with n degree of freedom to the right of t_\alpha(n) is \alpha: t_\alpha(n) is called a t critical value.

- Prop. A 100(1-\alpha)% confidence for the mean \mu of a normal population when the value of \sigma is unknown is given by

7.4.3 Large-Sample Confidence Intervals for a Popoulation Proportion

- Prop. A large-sample 100(1-\alpha)% confidence interval for a population propotion p is

where \hat p = x/n, x is the observed number of successes, and \hat q=1-\hat p. where \hat p = x/n, x is the observed number of successes, and \hat q=1-\hat p.

7.5 Precision and Sample Size

7.6 Inferences Based on Two Samples

7.6.1 Confidence Intervals for a Difference between Two population Means.

- Assumption.

1. X_1,X_2, ...,X_m is a random sample from a population with mean \mu_1 and variance \sigma_1^2.

2. Y_1,Y_2, ...,Y_n is a random sample from a population with mean \mu_2 and variance \sigma_2^2.

3. The X and Y samples are independent of one another

- Prop. The expected value of \bar X - \bar Y is \mu_1-\mu_2, so \bar X - \bat Y is an unbiased estimator of \mu_1 - \mu_2. The standard deviation of \bar X - \bar Y is sqrt{\sigma_1^2/m + \sigma_2^2/n}.

- Note. Provided that m and n are both large., a confidence interval for \mu_1-\mu_2 with a confidence level of approximately 100(1-\alpha)% is

7.6.2 The Two-Sample t tests and Confidence Interval

- Assumption.

1. Both populations are normal, so that X_1,X_2, ...,X_m is a random sample from a normal distibution and so is Y_1,Y_2, ...,Y_n(with the X and Y independent of one another)

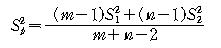

2. The values of the population variances \sigma_1^2 and \sigma_2^2 are equal, so that their common value can be denoted by \sigma^2.

- Def. The pooled estimator of the common variance \sigma^2, denoted by

S_p^2, is definde by

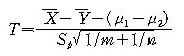

- Thm.

has a t distribution with m+n-2

d.f. has a t distribution with m+n-2

d.f.

- A 100(1-\alpha)% confidence interval for \mu_1-\mu_2 is

7.6.3 Inferences Concerning a Difference between Population Proportions

- Prop. Let X~B(m,p_1) and Y~B(n,p_1) with X and Y independent variables. Then E(\hat p_1 - \hat p_2)=p_1-p_2 and V(\hat p_1 - \hat p_2)=p_1q_1/m+p_2q_2/n.

- Note. A 100(1-\alpha)% confidence interval for p_1-p_2

Email: lbg@kowon.dongseo.ac.kr

ˇˇ |